China HEV expansion accelerates as Geely enters mass production and BYD NEV mix converges

China’s renewed focus on hybrid electric vehicles (HEVs) is expanding beyond initial technology announcements, with multiple automakers accelerating deployment plans following Geely’s i-HEV system reveal earlier this month. The shift builds on earlier signals from Chery and Geely, positioning HEVs as a parallel track to battery-electric vehicles rather than a replacement, according to China Automotive News.

Production rollout

Chinese automakers, including Geely and Chery, began repositioning HEVs as a strategic alternative to Toyota’s global hybrid dominance, with fuel consumption claims approaching 2 L/100 km under specific conditions.

This was followed days later by Geely’s official i-HEV system launch, which introduced a 48.4% thermal efficiency engine and reported fuel consumption below 4 L/100 km, alongside a Guinness-certified result of around 2.22 L/100 km under test conditions.

In the latest update, Geely has moved beyond the announcement phase, confirming that the i-HEV system has entered mass production deployment across key models, including Emgrand, Preface, Monjaro, and Boyue L, marking a shift from technology reveal to industrial rollout.

HEV systems driven by new tech

Across the industry, HEV development is increasingly defined by software-controlled energy management rather than mechanical power-split systems.

Geely’s i-HEV integrates AI-based control logic that continuously adjusts engine and electric motor output based on real-time driving conditions. The company describes this direction as part of a transition toward “AI-defined vehicles,” where energy flow is optimised dynamically rather than pre-set.

Changan and Chery are following similar paths, adopting series-parallel architectures and higher-output electric drive systems. Chery continues to expand its hybrid battery strategy, targeting a capacity of around 5 kWh, significantly above the 1–2 kWh of traditional HEV systems.

GAC has also joined the broader HEV restructuring wave through its Adimotion hybrid architecture, which integrates HEV+, plug-in hybrid, and range-extender systems into a unified platform.

The system reflects a shift toward scenario-based energy management, where multiple electrified powertrains are managed within a shared software and control framework rather than developed as separate architectures. This approach positions hybrid technology within a full-spectrum electrification roadmap, aligning with the industry-wide move toward more flexible, software-defined vehicle energy systems.

Great Wall Motor (GWM) has further expanded the hybrid landscape with the Ora 5 model, which marks a shift from a pure-electric positioning to a full multi-powertrain strategy covering BEV, HEV, ICE, and PHEV variants on a shared platform.

The HEV version features a 1.5-litre turbocharged engine paired with a dedicated hybrid transmission, reflecting a modular approach in which electrified and combustion powertrains are deployed within the same vehicle architecture. This positions GWM differently from peers focused on efficiency optimisation, as the company is emphasising platform flexibility across multiple energy types rather than a single hybrid efficiency pathway.

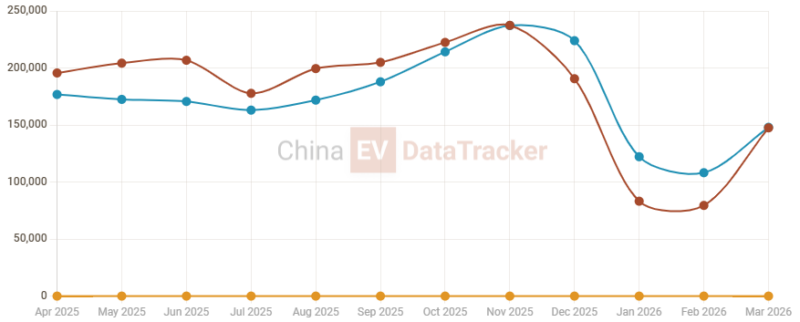

BYD data highlights internal NEV balance shift

Additional market context comes from BYD’s internal new-energy-vehicle sales structure, which excludes conventional HEVs but reflects a balance between battery-electric and plug-in hybrid systems.

In January 2026, BYD recorded 40.5% BEV and 59.5% PHEV sales. In February, the split shifted to 42.4% BEV and 57.6% PHEV. By March 2026, the structure reached near parity at 49.9% BEV and 50.1% PHEV.

This trend highlights a stabilising internal mix between fully electric and plug-in hybrid models within China’s largest NEV manufacturer, rather than a pure BEV-led structure.

Policy timing and global positioning

The HEV expansion is unfolding alongside China’s 2026 policy adjustment, which reduces purchase tax exemptions for battery electric and plug-in hybrid vehicles from full exemption to a 50% reduction capped at 15,000 yuan (about 2,070 USD). This narrows the cost gap between different electrified powertrains.

At the same time, Chinese automakers are increasingly positioning HEVs as part of export strategies, particularly in regions where charging infrastructure remains limited. This includes Southeast Asia and South America, where hybrid systems offer operational flexibility without dependence on charging networks.

Structural transition rather than replacement

China’s EV penetration surpassed 52% in March 2026, yet the expansion of HEV systems suggests that multiple powertrain technologies are evolving in parallel rather than sequentially replacing one another.

Rather than reversing electrification trends, the current phase reflects a multi-pathway structure where BEV, PHEV, and HEV systems coexist across different use cases, cost segments, and global markets.

![]()