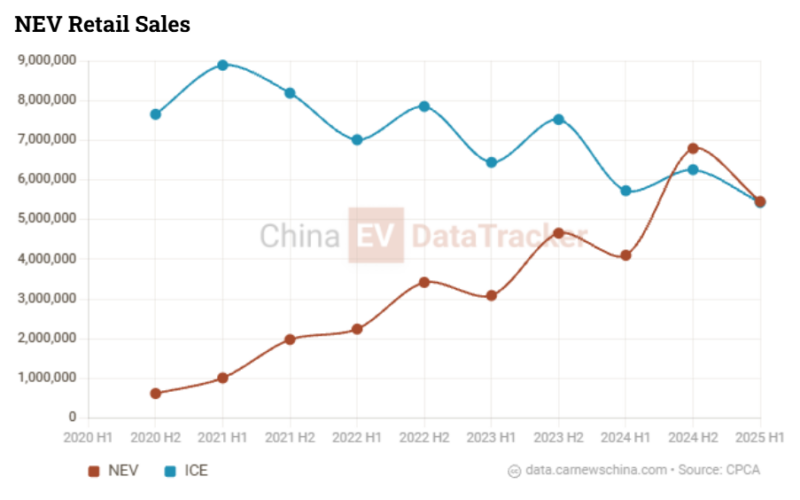

Passenger vehicle sales in the first half (H1) of 2025 reached 10,891,000 units in China, a double-digit growth of 10.7% year-over-year. The increase was driven by New Energy Vehicle (NEV) sales, which grew 33% to 5,458,000 units. The sales of traditional internal combustion engine (ICE) vehicles were down 5.2% to 5,433,000 units, according to CPCA data monitored by China EV DataTracker.

New Energy Vehicle is a Chinese term for EVs, which includes battery electric vehicles (BEVs) and plug-in electric vehicles (PHEVs). To be completely precise, it also includes hydrogen vehicles (FCEV), but their sales are nearly non-existent in China.

EV sales in China

All-electric vehicles were growing faster than plug-in hybrids in the first half of the year in China. BEVs increased 37.6% to 3,330,000 units, while PHEVs grew 26.5% to 2,128,000 units.

All-electric vehicles increased their share of NEV sales in China over plug-in hybrids. BEVs increased their share by 2 percentage points to 61% year-over-year, while PHEVs lost 2 percentage points to 39% share.

The NEV penetration of China’s passenger vehicle market surged to 50.1%, up 8.4 percentage points year-over-year, while ICE vehicle sales fell to 49.9% in H1 2025.

Lei Xing’s take: It’s too early to call the transition from PHEVs/EREVs to BEVs is over as we see the launch of large three-row battery electric SUVs led by the ONVO L90, Li Auto i8, Model Y L, AITO M8 and IM LS9, just to name a few, Xiaomi and Xpeng have yet to launch their EREVs or “super hybrids” or “super electrics,” and as shown from the Ministry of Public Security data on vehicle parc numbers that the share of BEVs of all NEVs actually deceased by more than a percentage point as of the end of June 2025 from the end of 2024.

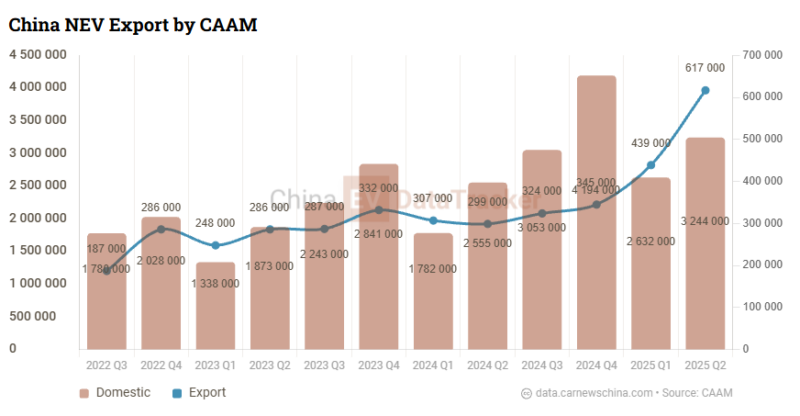

China NEV Export

For the first time in history, China exported over 1 million NEVs in H1. Exports reached 1,056,000, up 74.3% from 606,000 units in H1 2024, according to CAAM data, which, unlike CPCA data, includes commercial vehicles. Overseas sales accounted for 15% of overall China NEV sales. The export was mainly driven by Tesla and BYD.

Lei Xing’s take: While NEV exports continue to grow, PHEV exports are growing faster than BEV exports, mainly driven by regulatory factors (e.g., Europe).

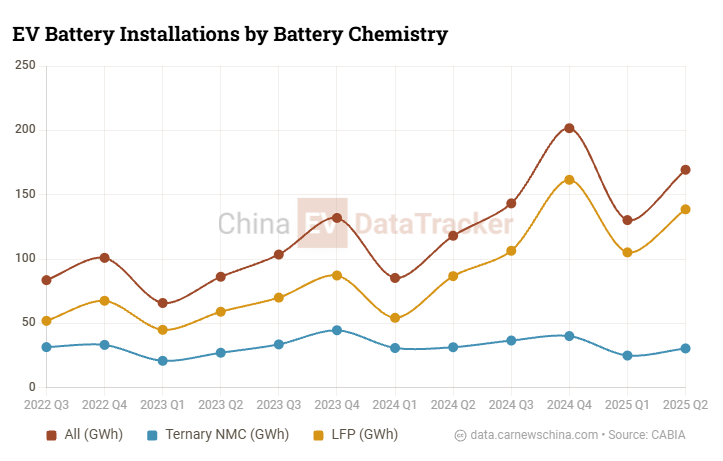

EV battery installations

In the first half of the year, 299.7 GWh battery capacity was installed in EVs in China, u 47.3% year-over-year.

The surge was driven by lithium-iron-phosphate (LFP) batteries, which increased 73% year-over-year to 243.9 GWh.

Meanwhile, ternary NMC battery declined 10.9% to 55.4 GWh. This continues the trend from H2 2024, when NMC battery installations declined for the first time in history year-over-year, by 1.9.%. Apparently, the era of NMC is over, and the age of LFP has begun. NMC will most likely remain on some upper-market vehicles; however, even there, their position is not secure, as, for example, the 90,000 USD Yangwang U7 with 960 kW (1287 hp) and 720 km range features an LFP battery from BYD.

In H1 2025, the LFP had an 81.4% share while NMC declined to 18.5% on China-made vehicles.

Lei Xing’s take: LFP is king and will dominate battery chemistry for the foreseeable future.

Battery production

A total of 697.3 GWh of batteries were produced in China during the first half of the year, representing a 62.2% year-over-year increase.

NMC production rose 13.5% YoY to 144 Wh, while LFP rose 82.9% YoY to 552.4GWh.

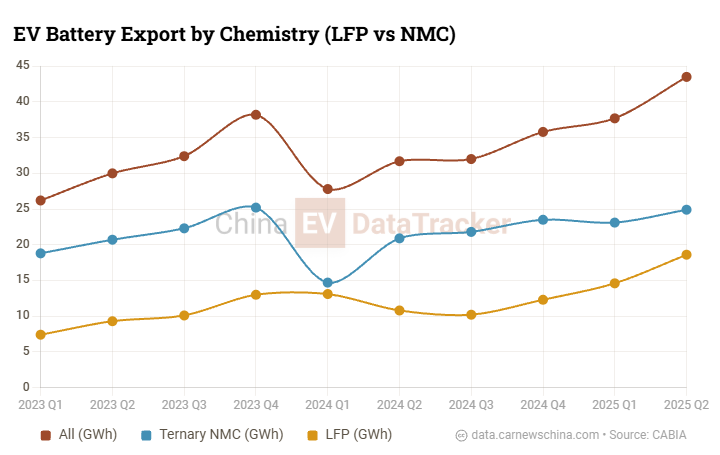

Battery export

A total of 81.2 GWh was exported to overseas markets, up 36.5% in H1 2025.

The export was driven by NMC batteries, which accounted for 59.1% overseas sales. LFP share is 40.9%.

China exports batteries for Energy storage systems and for Electric vehicles. For Energy storage, it exported 45.6 GWh, up 232.8 % year-over-year. Batteries for EVs rose 35.5% to 81.6 GWh.

The energy storage share is 35.8%, while the EV battery share is 64.1%.

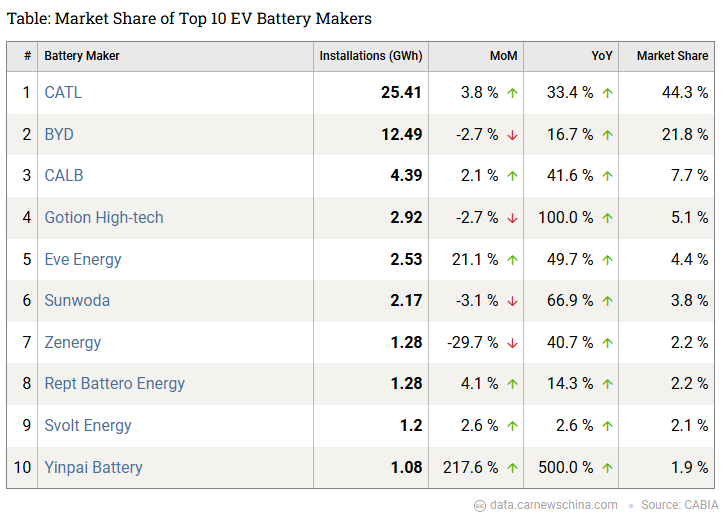

EV battery brands leaderboard

This is a quite boring part as nothing really changes here. As usual, CATL is first with a 44.3% market share. They installed 25.41 GWh of batteries into EVs, up 33.4% year-over-year.

BYD is second with a 21.8% share, having installed 12.49 GWh. However, their growth was at a slower pace than CATL – 16.7% up year-over-year.

Third was CALB, with a 7.7% share and 41.6% growth, and fourth was Volkswagen-backed Gotion High-tech, with a 5.1% share and 100% year-over-year growth.

Lei Xing’s take: It would be much more interesting to see the battle outside CATL and BYD, both in terms of market share as well as installation growth (e.g. CALB is expected to benefit from Xpeng’s volume growth as it’s the exclusive battery supplier)

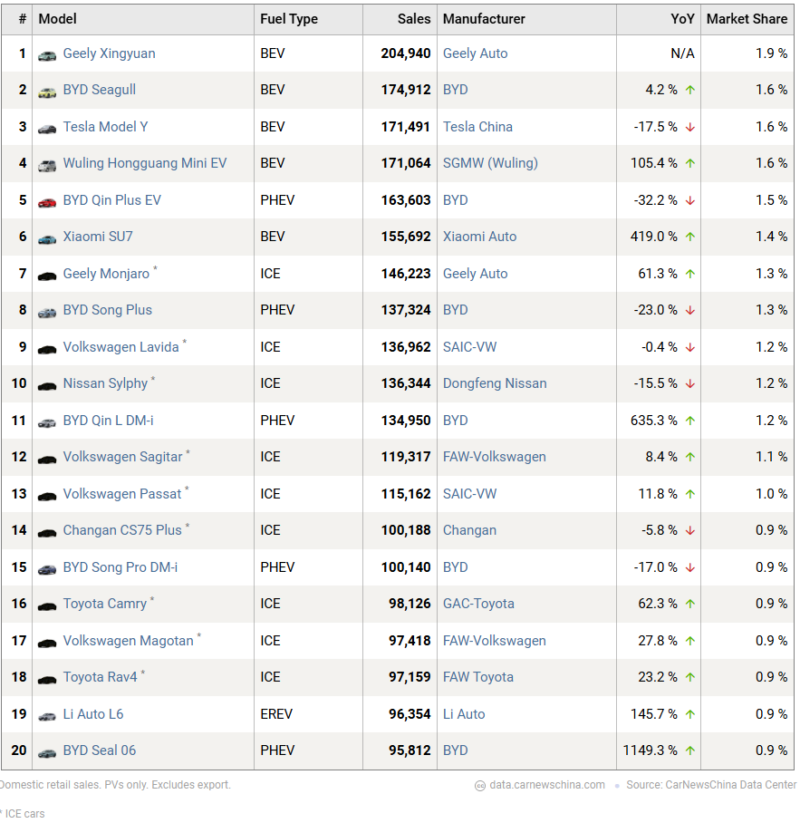

Best-selling cars in China

The compact hatchback Geely Xingyuan was the best-selling vehicle. However, year-over-year comparisons are not available as the 65,800 yuan (9,200 USD) EV launched only in October 2024.

Second place goes to BYD’s Seagull, again a compact hatchback and third place goes to Tesla Model Y.

The first spot goes to EVs, while the best-selling ICE is Geely Monjaro in seventh place, right behind the Xiaomi SU7 sedan.

Lei Xoing’s take: Geely Xingyuan being the top NEV seller, beating the BYD Seagull, is the surprise of the year, while Model Y remains relatively resilient. The top 10 by this time next year will likely all be NEVs, and all of them will be Chinese NEVs, except Tesla.

EVs on the road as of June 2025

As of June 2025, there were 359 million cars on the road in China. 10.3% of them, 36.9 million, were NEVs. Of those NEVS, 69.2% were all-electric, the rest were PHEVs. This is slightly down from 70.3% BEV share at the end of 2024.

Lei Xing’s take: For every 10 vehicles on the roads in China, one is an NEV, another major inflexion point as China enters the era where half of new vehicles sold are NEVs and a double-digit percentage of vehicles on the roads are now NEVs.

Those were the main snippets for H1 2025. The full monthly report is being delivered to the members of China EV DataTracker community.

![]()